Retail Chronicles | 07.07.2020

Emerging trends in retail and new commerce.

Hello, it’s Alexandre from Spring Invest, a French investment fund dedicated to RetailTech. Welcome to our last edition of Retail Chronicles, our bi-monthly newsletter about emerging trends in retail and new commerce.

💡 Direct-To-Consumer brands are evolving

Consider the current state of retail. With malls shuttering, retailers defaulting on rents, and foot traffic wavering, e-commerce has become one of the most reliable retail formats.

Therefore, major brands have begun discussing their own strategies to counter an evolving retail market and have begun scouting for direct brands.

The 5 attributes they are looking for are the following :

1. Profitability

2. Demonstrated omnichannel expertise

3. Organic marketing flywheel

4. A team that can continue to execute a savvy paid strategy

5.Founder-led with longer-term management potential

So, YES, profitability is back as the #1 priority.

On a related note, we have noticed that the greatest commonality for profitable DTC is a sustained Gross Margin %, which is far more lasting than a specific low cost of acquisition that is usually weakening over time as the audience saturates. Quoting a tweet from Digital Native, here is a good proxy to assess gross margins of DTC :

40-50% : Common/Weak

50-60% : Average

60-70% : Interesting

70-80% : Winning

80-90% : Dominant

90-99% : Cash Machine

🏆 TOP 50 e-commerce brands and retailers

The methodology is based on June 2020 business volumes (vs. May 2020 and June 2019).

One major trend is second-hand

The second-hand online market is booming and the COVID-19 crisis has even accelerated it, thanks to an expanding offer and services that are close to that of new products: user experience, design, high-quality photos, in-store payment, shipping, product return, etc. On Back Market, the level of professionalism is such that customers even forget that products are second-hand.

In such context, big winners are Vinted (n°3), Back Market (n°12), Ebay (n°15) and Le Bon Coin (n°19, +35 vs. last year). As an example, Vinted now captures significant shares of major brands second-hand transactions: Nike (10%), Adidas (13%), Ralph Lauren (22%), Levis’ (26%), and even 81% of the French brand Petit Bateau.

As a result, many brands are trying to fight back by creating their own second-hand online stores but none of them succeeded so far, the major problem being the cannibalization of their own offers if the store is a sublet the main e-commerce or the cost of acquiring decent traffic if built as a new store. Even Apple, which launched its own refurbished store 15 years ago, is losing market shares against Back Market that is now selling 25% of Apple’s second-hand products (in France).

Together with a demand that is also driven by environmental considerations, the market is booming and second-hand sales of equipment products (excluding food) now represent 9% of total online sales on a market estimated at 22Bn€, all categories combined.

The same is happening in the United States, with second-hand startups like ThredUp that said that from mid-March to the end of May, its weekly gross transaction volume has grown 20% compared to the same time period last year. Also, from mid-April to mid-May, Poshmark experienced a 50% increase in clothing and accessories sales compared to the previous year. Finally, Depop’s traffic increased 100% year-over-year in April.

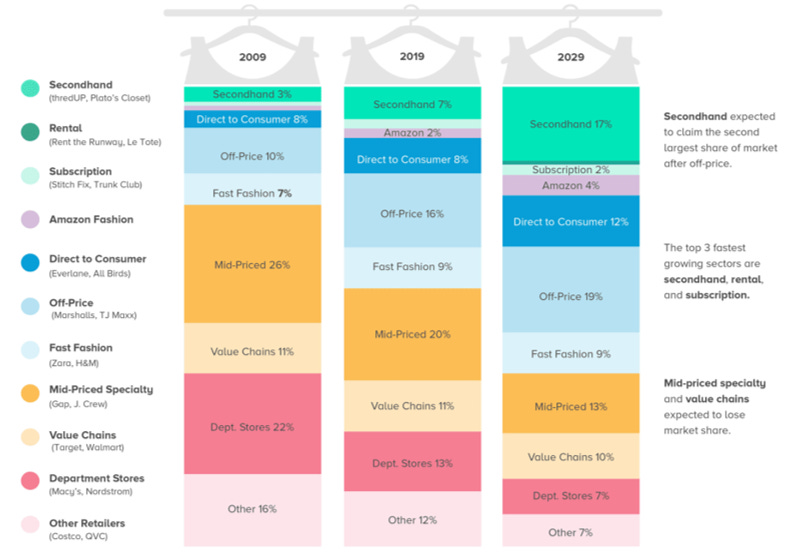

Finally, to better understand who will be the winners and losers of this trend, please meet the “closet of the future” by ThredUp :

🔥 With the depression, PRICE is now the consumer’s #1 concern.

What is happening?

25% of the French population has been impacted by the “chômage partiel” over the past few months, and more than 50% of them have suffered from a salary reduction. Even though the unemployment rate has remained quite stable over the past few months, it is expected to rise with projections showing 890,000 additional unemployed people in the next 18 months.

For low-wage workers (more than 5 million people), a 10% decrease in revenues means that their consumption will roughly decrease by 1/3. More precisely, the loss of earnings is estimated between 216€ (by Intermarché) and 240€ (by Leclerc), compared to an average monthly food budget of 385€.

15% of the population acknowledges having difficulties paying for their food and most of them have the feeling that “prices have gone up recently”. While data shows that prices have remained quite stable, it reveals that the price sensitivity has gone up significantly.

What are the consequences?

33% of shoppers admitted that they are now more attentive to consumer goods prices. The most impacted populations are families (43%) and those who have suffered from a decrease in working hours or unemployment (56%).

94% of the consumers now expect their supermarkets to “help them fight their decreasing purchasing power”. In other words, consumers expect reduced prices and special offers. As in many crises before, the price is becoming the #1 concern. The study also shows that the quality of products comes down as #2 and the engagement for social and environmental matters as #3.

Food distributors have therefore decided to focus their communication on prices. For example, Intermarché and System U have already announced that prices will be frozen until September. Also, as in 2008, the crisis should benefit to store brands and discount distributors.

🛒 Fresh news from the food retail

Carrefour is launching its marketplace. Lidl might do the same.

C’est qui le patron opens its first drive/store. Two more to come in Paris and Dijon.

Auchan has decided to remove all plastics from the fruit & vegetable shelf.

Franprix partners with Decathlon to open 100 corners.

Chronodrive partners with Direct Market to offer short circuit fresh foods.

🔎 Retail apocalypse: behind the scene.

Alinea, Naf Naf, Andre, Camaieu, Les 3 Suisses, Célio, La Halle,... you have certainly heard about all of these companies facing financial difficulties.

What is happening and why?

First of all, the economic model of physical retail was already under stress before Covid-19 with relatively weak growth, very strong pressure on prices and margins, and high fixed costs often representing half of the turnover. Under these conditions, the level of operating margin turns out to be very limited while working capital requirements weigh heavily on cash. See below what a typical income statement looks like for these companies, showing Ebitda Margin between 3 to 4% on average in the industry.

As a result, the economic equilibrium is very sensitive to the drop in turnover per store and per square meter. On average, a drop of 5% in the frequentation of a store leads to a drop in the operating margin rate of 2 to 3 points.

So why not going into e-commerce?

Many have tried, very few succeeded. Also, much has been written about the difficult transformation of the players involved in physical commerce, but the heart of the problem is that e-commerce is a completely different job, not just an additional distribution channel.

Distributors have reached an unparalleled level of expertise in product selection and management of a wide network of stores. But these skills are just not relevant in e-commerce. The constraints and the business model are different.

Moving from physical commerce (limited space, local shoppers, high fixed costs, field operations, human management, etc.) to digital retail (unlimited space, economies of scale, high variable costs, digital acquisition, etc.) requires learning a completely new job.

In addition, most of these historic players use legacy technologies at all levels of the chain (production, logistics, supply, point of sale, payment, CRM, etc.). This complicates the interfacing required for the integration of an e-commerce channel, which usually results in long and costly projects with multiple stakeholders.

Finally, there is the innovator’s dilemma and the fear of cannibalizing sales that could generate “channel conflicts”, as with Levi’s in 1999, who had finally decided to withdraw from e-commerce.

👍 If you like Retail Chronicles and want to help it grow, please share this newsletter with your colleagues, followers, and friends. If you hate it, then send it to your enemies. Have a great day, and see you soon!

About us

Spring is a French investment fund dedicated to companies that are shaping the future of retail. We invest both in Enablers, B2B companies providing innovative solutions to (e)retailers, and Disrupters creating new models of distribution. Our investment approach relies on strong relationships with 50+ European Retailers in order to provide sales acceleration to our portfolio. We also provide operational support with a dedicated team of Venture Partners working with our portfolio on sales, communication, HR, and internationalization.